When applying for trade credit insurance, a prospective insured will typically provide information on the financing arrangements that will form the basis of cover. Where there is deviation from these financing arrangements, questions can arise as to whether the policy will respond.

The New South Wales Court of Appeal considered this situation in BCC Trade Credit Pty Ltd v Thera Agri Capital No 2 Pty Ltd [2023] NSWCA 20, concluding that while the insured provided credit other than in accordance with the agreed financing structure, the loss that arose nevertheless came within the scope of cover.

The judgment also provides comment on how instances of fraud are to be interpreted where the insured is the victim of “sham” trade documents.

Background

In February 2020, Thera Agri Capital No 2 Pty Ltd (Thera), an Australian credit financier, entered a credit facility with two companies within the Phoenix Group (Phoenix) for the purchase of grains and pulses. The credit facility was guaranteed by holding company Phoenix Commodities Pvt Ltd (Phoenix Commodities).

To comply with Sharia law, parties financed the transactions by way of a Sharia-compliant Master Murabaha Contract.

Thera entered a trade credit policy with BCC Trade Credit Pty Ltd (BCC) to cover the refusal or failure of the guarantor (Phoenix Commodities) to honour its debt obligations in accordance with the guarantee.

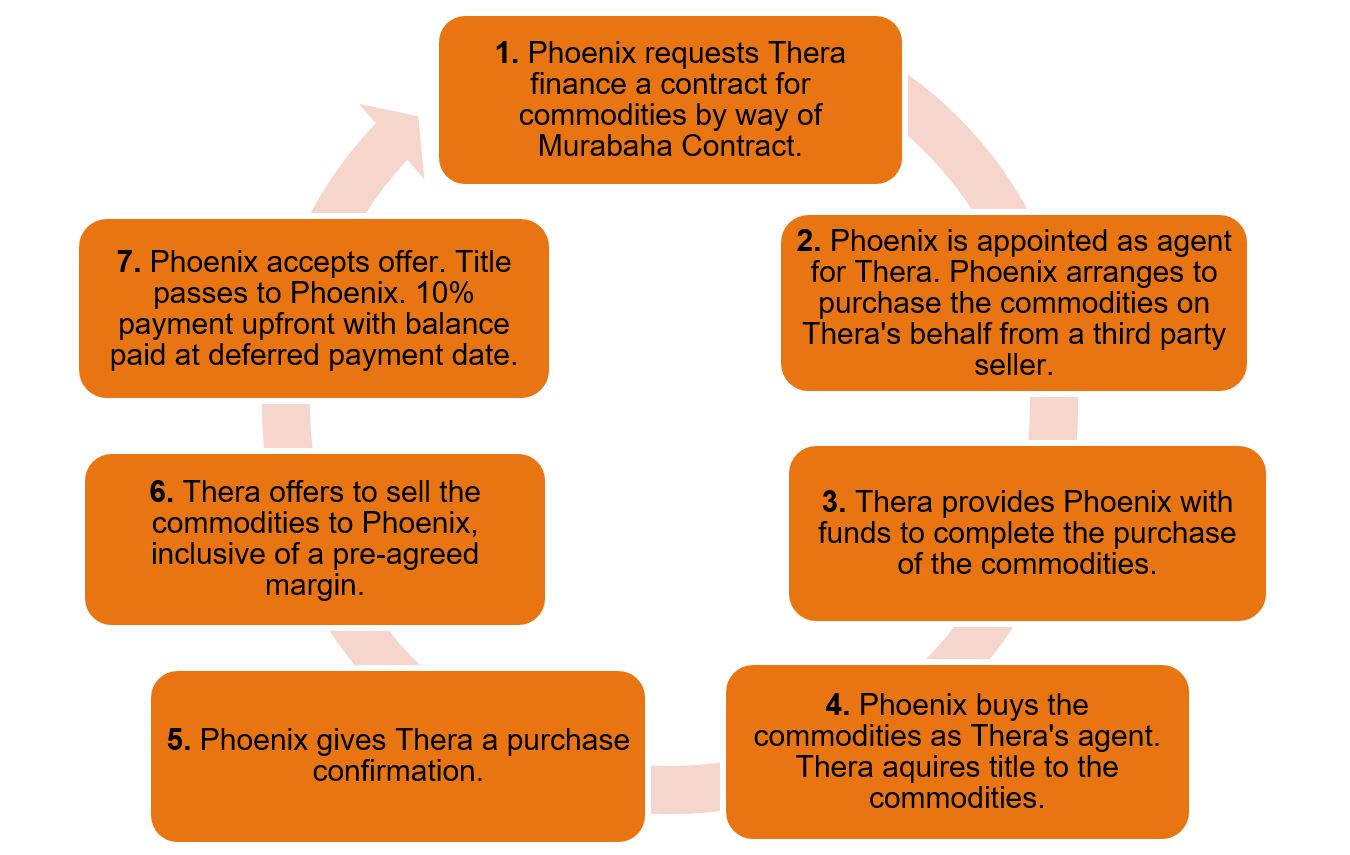

The financing arrangement between Thera and Phoenix was structured as follows:

While Thera advanced AUD 8 million to Phoenix for purchase of the commodities, the transaction departed from the arrangements above. The contracts for the purchase of the commodities between Thera and Phoenix preceded the drawdown requests, with Phoenix never purchasing the commodities as agent of Thera.

Shortly thereafter, Phoenix Commodities went into liquidation followed by Phoenix. No repayments were made to Thera.

It was later uncovered that unbeknownst to Thera, the underlying trade documents were shams. While the commodities existed and had been shipped under bills of lading, they were not in fact the subject of the purchase between Phoenix and the third-party supplier.

Thera sought indemnity under its policy with BCC. BCC rejected the claim on the basis that: (a) the advances had not been made in accordance with the Murabaha Contract; and (b) the documents provided by Phoenix to secure financing were “shams”.

Thera was successful at first instance, with the Court concluding that Thera’s deviation from the credit facility structure did not take the transactions outside the scope of cover. BCC appealed the decision.

Judgment

The Court of Appeal issued judgment in favour of Thera, dismissing the appeal.

Thera argued it advanced funds to Phoenix under enforceable contracts (albeit not contracts that complied with the Master Murabaha Contract). Accordingly, Phoenix Commodities incurred a debt obligation which it failed to discharge, bringing it within the scope of the policy.

BCC contended that “debt obligations” was not a generic liability for any debt incurred by Phoenix Commodities, but rather referred to a specific liability that arose under set of structured transactions and a risk that Phoenix Commodities might fail to honour the obligations created by that arrangement.

Majority Decision

The majority agreed with Thera and the court of first instance, with Macfarlan JA noting that:

“It is not in my view important that the transaction documents were not executed in the sequence contemplated by the Master Murabaha Agreement or that there were anomalies in terms of the times at which events occurred. What is important is that the Insured’s and the Counter-Party’s [Phoenix] contractual documents were genuine (that is, not shams) and that they provided that as between those parties their contractual regime accorded with the basic elements of the Master Murabaha Agreement.”

Additionally, it rejected that cover should be excluded on the basis the underlying trade documents were shams. Thera was innocent of the fraud and had entered into genuine contracts with Phoenix. It applied objective contractual principles noting “a fraudulent intention of only one party to the contract, uncommunicated to the other, does not suffice to render the contract a sham”. This interpretation was consistent with the policy exclusion for loss arising out of “the fraudulent, dishonest or criminal acts of the Insured”.

Dissenting Opinion

Basten AJA reasoned that Phoenix did not operate as Thera’s agent because the purchase contracts were entered into before execution of the finance documents. Instead, Thera can be said to have advanced funds to enable Phoenix to purchase the commodities on its own behalf. Thera, having obtained no title to the commodities, could not pass title to Phoenix and so Phoenix had no payment obligations arising “in accordance” with the Murabaha Contract.

He concluded the policy “did not accommodate such a broad statement of purpose” to respond to a default arising outside of obligations created by the credit facility, which was presented to BCC at the time of inception and material to the insuring clause.

Our Comment

While it will depend on the circumstances and policy wording to apply, the judgment indicates a trade credit insurer may be required to provide cover even where there has not been strict compliance with the financing arrangement presented at inception, provided the insuring clause can be sensibly read to respond.

It also provides guidance on how instances of fraud are to be interpreted in a credit insurer’s policy, with loss arising from the dishonest acts of persons the insured has contracted with being the very type of loss a credit insurance policy is expected to respond to.

If you have any questions about credit insurance or policy interpretation, please get in touch with our Trade & Transport Team or your usual contact at Hesketh Henry.

Disclaimer: The information contained in this article is current at the date of publishing and is of a general nature. It should be used as a guide only and not as a substitute for obtaining legal advice. Specific legal advice should be sought where required.